In the current environment with excess liquidity is harder and harder to identify good value investment opportunities. However, I see below are a good value pharma company with nice prospects.

Zhongzhi Pharmaceutical Holdings Ltd (3737)

Sector: Biotechnology & Drugs

Price (June 5th., 2021): HK$1.41

Target price (12m): HK$1.9

Dividend Yield: 2.6%

Expected Share Price Return: +35%

Investment Risk: Medium

Rationale for investment

- Market size is to expected to grow at 20% p.a. over next years driven primarily by increasing global demand for Chinese medicine;

- Cheap valuation – company trades at a P/E of 7x versus an industry average of 20x

- Well established brand in the local pharmaceutical industry enabling to generate high profit margin from own-branded modern decoction pieces.

Profile

Zhongzhi Pharmaceutical Group is researching, producing, selling the traditional Chinese medicine preparations, prepared slices of Chinese crude drugs and foods. It was listed on the Hong Kong Stock Exchange in 2015 (Stock code: 3737 HK). They own 201 self-operated chain pharmacies selling both own-branded products and other types of other pharmaceutical products, healthcare products and medical devices sourced from independent suppliers. Revenue derived from the Guangdong province represented over 60% of total.

Chinese patent medicines are manufactured with Chinese herbs as major ingredients. The products are in various forms, such as oral solutions, pills, capsules, powder and syrup.

Investment Case

Chinese medicines have been widely used by the Chinese community for prevention and treatment of diseases as well as health enhancement for more than 2,000 years and have been increasingly popular. The Chinese medicine markethas experienced rapid growth. The total production value of Chinese medicines is expected to further increase at a CAGR of approximately 20% p.a. Such remarkable growth is primarily driven by the increasing global demand on Chinese medicines.

The living standards of PRC residents are gradually improving along with the economic growth and the increasing disposable income. Threatened by the outbreak of epidemics, the PRC residents are getting more healthconscious and they are willing to increase their spending on pharmaceutical and healthcare products including Chinese medicines, for prevention of diseases and health improvement.

The Group devote its best effort and resources to cope with the increasing market demand. In particular, the Group has commenced the construction of new factories premises and additional production lines in Zhongshan and Yunfu, Guangdong province, for the expansion of production capacity to cater for the increase in demand of the Group’s products. It is expected that the construction of the new factory premises will be completed by the end of 2021.

Valuation

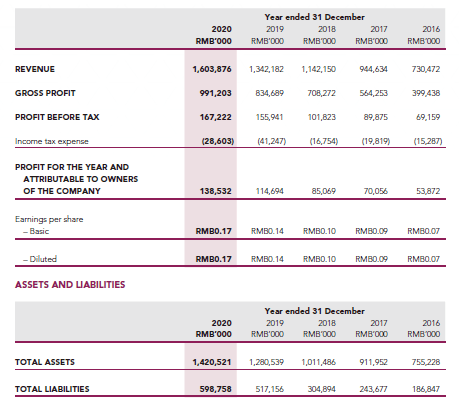

The company trades at a P/E of 7x versus an industry average of 20x. The high discount is not justified by gross margin at 62% which is higher than the sector one at 48%. ROE of 17% is in line with the sector at 16% for year ended 31 December 2020.

In 2020 revenue rose by 19.5% to approximately RMB1.6bn, Profit increased by 21% to RMB138m due to the strong growth momentum of the modern decoction pieces, stricter controls over costs as well as from slight adjustments in sales modes. There is limited public information on the financial outlook. Based on historical trend and market studies, I expect a 20%+ profit growth in 2021.

I make a quick and dirty estimate that the P/E multiple should increase to reach 10x representing, 50% of the industry over the next one year, which translates into a target price of HK$2.4. I further apply a 20% discount for being small player in emerging market hence I arrive at a target price of HK$1.9. The company paid a dividend of HK$0.037/share in for 2020 and I expect to be at least maintained.

Investment Risks

- Success is dependent on core brand ‘‘Zeus” and any negative publicity would adversely affect our operating results and financial condition;

- Revenue was mainly generated from the Guangdong province, the PRC. Any adverse change in the economic, political or social conditions in the region may materially and adversely affect business;

- Gross profit margin in the future may be adversely affected if the proportion of the sales of our own-branded product decreases.

Source: Company site, Annual reports, IPO Prospectus, http://www.investing.com

I or my affiliates may hold positions or other interests in securities mentioned in the Blog. Please see Disclaimer.

If you love the articles I write, follow my blog and never miss another investment opportunity!

1 thought on “Leading Player In Chinese Medicine (Zhongzhi Pharmaceutical), June 2021”