SUNRUN (NASDAQ: RUN)

Sector: Electrical Equipment (Residential Solar Panels)

Price (Jan. 14th., 2022): $31.8

Target price (12m): $41

Expected Share Price Return: +29%

Investment Risk: Medium

Rationale for investment

- Residential solar market has low penetration

- Industry leader with meaningful scale advantages and 14-year track record

- Recurring revenue model with low churn

- High top-line growth with strong margins and ability to cross sell and up sell to existing customers

Profile

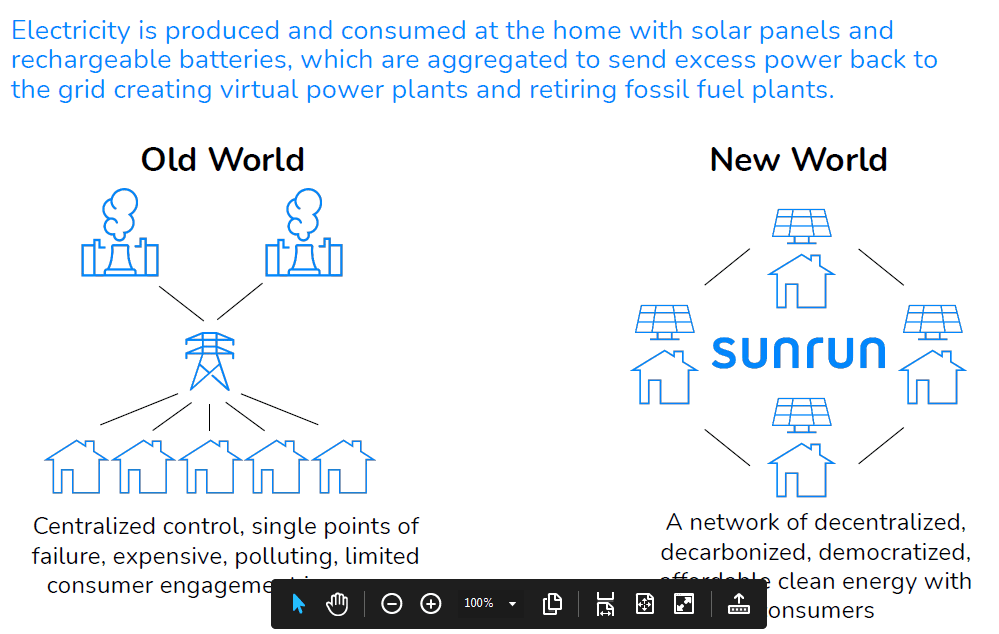

Sunrun Inc. is a home solar, battery storage, and energy services company. The Company is engaged in the design, development, installation, sale, ownership and maintenance of residential solar energy systems in the United States. It has 630,000 customers and has sold solar service in 22 states, DC & Puerto Rico.

Company provide a solar energy service with fixed pricing under 20- or 25-year agreements that generate recurring, contracted revenue for multiple decades with an experienced loss rate of ~1%.

Investment Case

This is one of the rare companies in my model portfolio that is not profitable yet, but I see it turning to profit in 2022.

Sunrun is the #1 residential solar market leader and yet remains <1% of total US residential electricity market. There is a strong momentum for growth and margins for such a company- cost of electricity has increased 3% per year on average from 2004 through 2020; the costs of solar modules and batteries have declined significantly over the last ten years – market research forecast the cost of installed solar panels will decline 34% while the cost of batteries declines 64% over the next 10 years (Source: Wood Mackenzie Research, California Solar Statistics, Bloomberg New Energy Outlook 2019).

There is an urgent need to address climate change and the public is very supportive. Moreover, electric vehicle sales are growing and there are synergies with onsite generation and energy management of electric vehicles.

Valuation

My Dec 2022 price target is $41, based on an assigned Price/Sales multiple of 4.4x of my FY23 sales estimate of ~$1.9bn. Industry database exhibits a P/S for Electrical Equipment sector of 3.7x. (source: Damodaran site) and I added a 20% premium to 4.4x for Sunrun being market leader on a high growing segment of the industry.

Investment Risks

- Policy and regulatory risk – Federal, state, and local authorities are positioned to terminate or retroactively reverse tax credits, renewable energy credits, and other incentives or impose charges on rooftop solar customers who want to connect to the grid;

- Market risk – Residential solar market growth could slow relative to expectations or shift toward homeowners making outright cash purchases that bypass the lease, PPA, and loan options;

- Competition- Sunrun faces head-on competition from other national residential solar service companies and a host of regional and local companies.

I or my affiliates may hold positions or other interests in securities mentioned in the Blog. Please see Disclaimer.

If you love the articles I write, follow my blog and never miss another investment opportunity!

2 thoughts on “Building the Future Electric Grid (SUNRUN), Jan. 2022”