ILLUMINA (ILMN)

Price (01 Feb 19): $280

Target price: $330

Expected share price return: +18%

Market Cap: $41bn

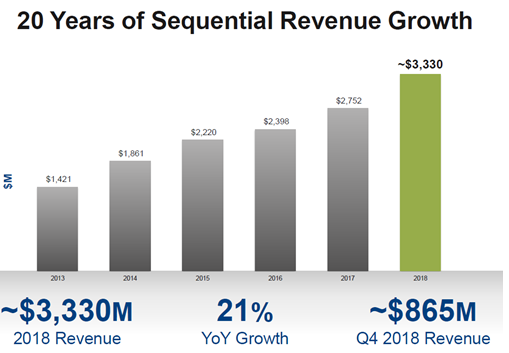

Illumina (ILMN), listed on NASDAQ, is a leading developer, manufacturer, and marketer of integrated systems for large-scale analysis of genetic variation and function. These systems are enabling studies that were not even imaginable just a few years ago, and moving us closer to the realization of personalized medicine. The Company provides reproductive-health solutions, including noninvasive prenatal testing, preimplantation genetic screening and diagnosis, and neonatal and genetic health testing. Their customers include a broad range of academic, government, pharmaceutical, biotechnology, and other leading institutions around the globe.

Rationale for investment

Illumina enjoys a Gillette like razor-blades business model featuring secular growth. While the company makes a lot of money from instrument sales, 50-60% of its revenue came from consumables sales. NovaSeq consumables revenue is growing with an increasing number of systems installed. However, many of the NovaSeq customers have transitioned from Illumina’s HiSeq high-throughput sequencing system. HiSeq consumables revenue is therefore falling. Over the long run, NovaSeq should drive higher overall consumables revenue, but there was could be some slow down in the near term in a context of a secular double digit growth, which is a good entry opportunity in a growth stock..

Valuation

ILMN issued 2019 guidance in Jan. 2019 which included revenue growth of 13-14% and non-GAAP EPS of $6.50-6.60. My $330 PT is derived by applying a 50x P/E multiple to company forward 2019 EPS estimate of $6.50. The multiple reflects a return towards levels reached during the last major new product cycle (HiSeq X). My target multiple captures the growth potential and early momentum of ILMN’s recent NovaSeq system launch.

Source: https://emea.illumina.com/content/dam/illumina-marketing/documents/company/investor-relations/ILMN-at-JPM-2019-7-January-2019.pdf

Investment Risks

- Primary risk is that market expectations are ahead of the pace of the ILMN business. Among headwinds we mention clinical opportunity, utility and reimbursement;

- The biggest issue that will hold back consumables revenue is the impact of trade tensions between the U.S. and China. So far, the only tariffs that have been imposed on the company affect its instruments;

- Some fields where Illumina operates or may operate within can be litigious. Factors such as these could inject elements of uncertainty into the mkt dynamic and slow demand.

If you love the articles I write, follow my blog and never miss another investment opportunity !