Fosun International Limited (00656.HK)

Price (08 Feb 19): HKD 11.8

Target price(12m): HKD 18.5

Expected share price return: +57%

Expected Dividend Yield: 3%

Market Cap: $85bn

Fosun International Limited is a Chinese investment holding company

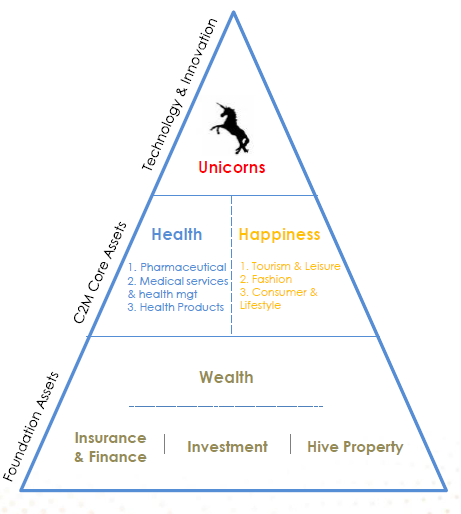

listed on the Hong Kong Exchange (00656.HK) operating diversified businesses. The Company manufactures steel, develops property, manufactures pharmaceuticals, holds interests in retailers, financial services providers and mining. Fosun’s mission is to create customer-to-maker ecosystems in health, happiness and wealth for families around the world.

Major portfolio companies in the ecosystem of Fosun include:

1) Health Ecosystem: Fosun Pharma, Sinopharm, Fosun United Health Insurance, Portugal’s hospital chain Luz Saúde, and one of the largest Indian pharmaceutical companies Gland Pharma;

2) Happiness Ecosystem: One of the world’s largest leisure vacation chains Club Med, Atlantis Sanya, Yuyuan Inc., and the top brand of Dead Sea mineral Israeli skincare brand AHAVA;

3) Wealth Ecosystem: Portugal’s largest insurance company Fidelidade, Portugal’s largest listed bank Banco Comercial Português (BCP), the German renowned private bank Hauck & Aufhäuser (H&A), Hong Kong-based Peak Reinsurance and Mybank.

Rationale for investment

We notice the group’s effort to listing more assets in the public market as a way to bring greater transparency to individual businesses and clarity to their valuation and reduce the discount. For now, c. 10% of its NAV is attributed to listed companies. Company announced that they will spin-off and separate listing of its wholly owned subsidiary Fosun Tourism and Culture Group. Moreover, Babytree, the largest parenting e-commerce platform in China, has also recently filed the listing application to Hong Kong Exchange.

Valuation

It is difficult to value Fosun given the significant number of its investments, many of which are unlisted. Company trades at a non-demanding P/B ratio of 0.9 and a P/E ratio of 6. Current price, at the latest reported Adj.Net Asset Value (NAV) of HKD30.78, translates into a discount to NAV of 62% . There are various factors affecting the levels of NAV discount the Asian conglomerates trade. In general, those providing better disclosure, transparency on their strategies and having more listed assets trade at a narrower NAV discount.

I believe value unlocking through accelerated asset divestment/IPOs should drive a re-rating of the stock to a discount to NAV of 40% (as a reference average discount in the last 10 years was c. 32%). This should translate into a target price of HKD18.5.

Risks:

- Global slowdown of the economy;

- High volatility stock;

- Corporate governance and political risks in China

- Sharp interest rate hikes.

2 thoughts on “Health, Happiness and Wealth at a Discount (Fosun International Ltd.)”