British American Tobacco plc (BATS/BTI)

Price (3 May 19): US$38.14 / GBB28.97

Target price (12m): US$54.5 / GBP41.4

Expected share price return: +43%

Dividend Yield: 7%

Expected total return: 50%

Market Cap: $2.4bn

Investment Risk: medium

Rationale for investment

• Strong financial results over the last 10 years;

• Sustainable dividend yield of 7% pa;

• BAT combustible products continue to outperform the industry;

• New product categories should enhance profitability.

British American Tobacco (BATS / BTI) is a tobacco and next generation products company with a business mix that is heavily exposed to emerging markets. It offers investors a combination of strong brands, good management, resilient earnings and dividend growth. The company is listed in UK and US.

Share price underperformance over the past 12 months (down 27%) was led by deteriorating investor sentiment on the back of combustible cigarette declines, new generation products disruption fears, regulatory news flow and rising interest rates. Performance was also not helped by the depreciating currencies across key markets versus USD.

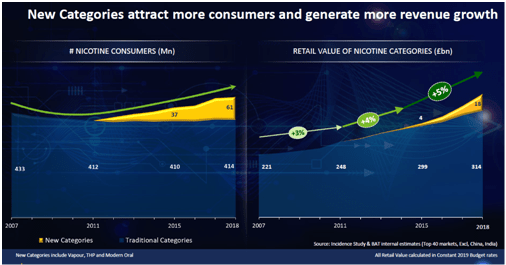

The sell off presents long-term investors with an excellent buying opportunity. The combustibles portfolio, although it was in a structural decline, generates significant free cash flow which funds a growing, substantial dividend. Simply valued on these free cash flows, British American Tobacco is an attractive investment. Company also plans $5bn revenues from new products by 2022.

Valuation

Revenue growth is estimated to continue at rates of 3-5% pa and operating margins of 42.5% in 2018 should increase by 50-100 bps this year (new generation products have higher margins). Management also estimate high single digit profit growth in the next years.

BAT’s ability to deliver organic revenue growth is superior to some of the European staples that are trading at 2xBAT’s 2019E P/E multiple. BAT currently trades on 11x 2019E P/E vs. industry average of 21x.

Tobacco peers (PMI, JTI) trade at at average 2019E P/E of 14, close to a decade low.

My 12m price target of GBP41.4 (+43% upside) is derived using a 5% discount over Tobacco peers 2019E P/E and BAT 7%+ sustainable dividend yield is there to stay.

Investment Risks

• Regulation, litigation, lower-than-expected growth in new products;

• Unfavorable FX (USD appreciation vs. world);

• Continued investor rotation out of companies with relatively high debt ratios;

• New legislation to increase the legal tobacco age to 21 is US under discussion.

I or my affiliates may hold positions or other interests in securities mentioned in the Blog. Please see Disclaimer.

If you love the articles I write, follow my blog and never miss another investment opportunity !

1 thought on “Robust Dividend by Transforming Tobacco Industry (British American Tobacco)”