Tesla (TSLA) is one of the most covered and controversial stocks. If you think Tesla would have sales like VW and margins like Apple in ten years by producing and operating electric self driving vehicles and unique energy assets then you should not agree to my story and valuation. If you are optimistic about electric vehicles and admire Mr. Elon Musk like me, please find below my humble opinion on the stock.

Tesla Inc. (TSLA)

Sector: Auto & Energy Products and Services

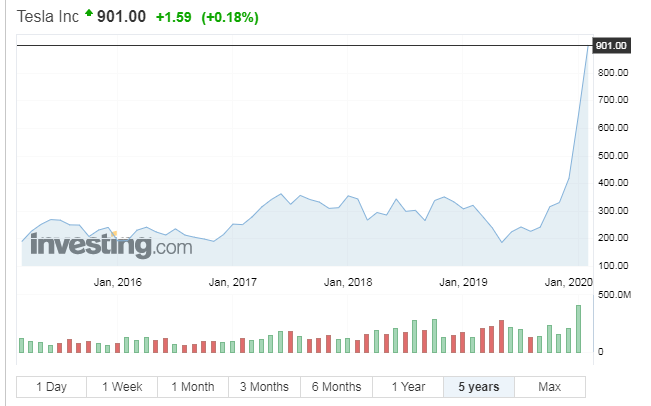

Price (Feb.23rd, 2020): US$901

Target price (12m): up to US$696

Expected Share Price Return: -29% (negative)

Investment Risk: High

Why Selling TSLA Stock Is Good Idea

- My Target Price in an optimistic scenario for TSLA stock is slightly below US$700 (-30% Downside) – see Valuation Section;

- There is a high probability for error in the execution of TSLA business plans in which case financing may dry up and sentiment will change;

- To ramp up production TSLA will require more capital creating significant negative cash flows in the near years;

- In my opinion market and Tesla funs underestimates the know-how of incumbent auto producers to deliver electric/self driving vehicles, which can make Tesla less significant (General Motors, VW, Google and Ford are quite advanced).

Tesla, Inc., formerly Tesla Motors, Inc., designs, develops, manufactures and sells fully electric vehicles, and energy storage systems, as well as installs, operates and maintains solar and energy storage products.

Valuation

An optimistic scenario is that Tesla consolidates its hold on the electric car market and will continue to grow that market, at the expense of conventional car makers. Pushing its production towards 2.6 million cars by 2030, it will also be able to deliver higher margins than conventional auto companies in steady state. While other revenue sources (green energy, driverless cars in ride sharing) will grow significantly (+25% p.a.) and supplement revenues, it will remain at its core an electric car company. I performed a quick and dirty valuation of TSLA using EV/Sales multiple appropiate for a high growth company.

My Key Valuation Assumptions (Optimistic Scenario)

- Electric Vehicles (EV) overall market will grow by an impressive 21% p.a. by 2030;

- TSLA sales will reach $125bn in 2030 from $24.6bn currently;

- Tesla market share in terms of number of vehicles will remains constant at 11%;

- Average price for TSLA cars will fall to USD30k following mass market adoption;

- TSLA other energy products and services (self driving cars, energy services and products etc.)will increase by a staggering +25% p.a. for the next 10 years;

- EV/Sales valuation for TSLA will be 5.3x (an average between and auto producer and a technology company) by 2030;

- I estimate the probability of failure of Tesla plans at 10%.

Risks for Selling TSLA Stock

- Short position should include a Stop Loss level. I would close the short position if stock increase to US$990;

- Autonomous driving will pick up and TSLA may remain the undisputed leader despite many contenders – GM, Google, Ford, VW etc.

- Tesla brand remains a cult for many people (investors and customers) and they may continue to behave irrationally keeping valuation high for long time.

I or my affiliates may hold positions or other interests in securities mentioned in the Blog. Please see Disclaimer.

If you love the articles I write, follow my blog and never miss another investment opportunity!