NAC Kazatomprom (KAP LI)

Sector: Uranium Mining

Price (05 Feb 20): $13.3

Target price: $18.8

Expected share price return:+41%

Dividend Yield (2020e): 6%

Total estimated return:+47%

Investment Risk: Low

Market Cap: $3.5bn

Following my initial post on the subject company in Jan. 2019, I updated my valuation and increased the target price from $16.7 to $18.8.

Profile

NAC Kazatomprom is the world’s largest uranium producer, commanding a 20% share of global supply with priority access to one of the world’s largest resource bases. Company is listed on London Stock Exchange in form of GDR and at Astana International Exchange.

Rationale for investment

- World’s largest producer of natural uranium with priority access to one of the world’s largest resource bases and 2nd lowest cost producer;

- Close proximity to Southeast Asian markets, incl. China, the fastest growing market for civil nuclear power;

- Stable Dividend Yield – estimated at 6%+ at current price

- National uranium operator – has preferred rights to develop any uranium deposit in Kazakhstan; State support.

Valuation

KAP is currently trading on 2019E EV/EBITDA of circa 9x, a ~36%+ discount to its closest comparable listed peer Cameco (Canada), which is traded at 14x multiple. I was right in my estimate that valuation discount will narrow over time. The discount in EV/EBITDA valuation between the two global players has reduced from 70% to 36% over last year. Unfortunately uranium price remained low and the outlook grim and all uranium producers valuation suffered. KAP returned only 3% total return in one year.

Going forward, I see an EBITDA of circa KZT190bn ($491m) in 2019E and KZT264bn ($687m) in 2020E. I estimate the current multiple of 9x2020E EV/EBITDA to remain the same as the company deserves a discount versus Cameco (Canada). EBITDA improvements should translate into an upside of 41%, respectively a Target Price of $18.8.

Company has an attractive dividend policy with minimum 50% FCF payout (provided ND/EBITDA<1.5x) & a $200m dividend floor. This translates into aprox. 5.8% dividend yield payable in 2020.

Uranium Price

Given the move toward cleaner energy, reduced carbon emissions, and more secure long-term energy sources, uranium supply is becoming more important to utilities worldwide. Currently, in our post-Fukushima demand case, uranium demand is projected to increase by 9% through 2030, according to UxC.

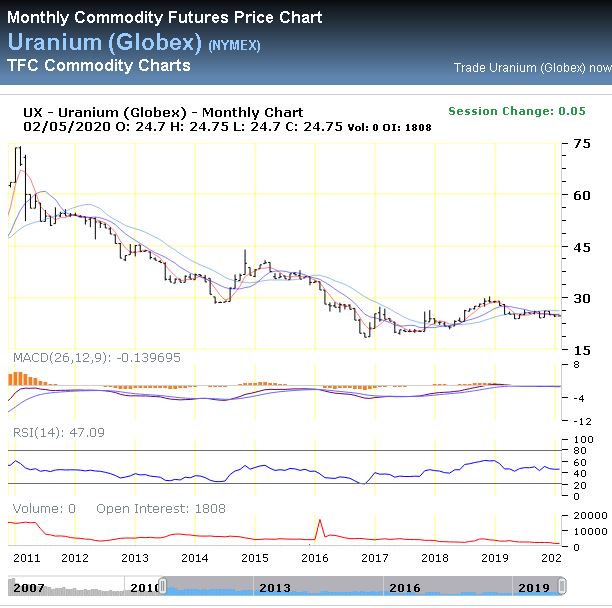

Uranium does not trade on an open market like other commodities. Buyers and sellers negotiate contracts privately. As per the chart below, current price of $25 does not look too high from istorical perspective. Uranium price declined by 24% in 2019.

Source: http://futures.tradingcharts.com/chart/UX/M?anticache=1548242279

Investment Risks

- Uranium price sensitivity- uranium mining segment accounts for c. 80% of group revenue and earnings;

- Global nuclear industry bears specific environmental, social and governance (ESG) risks;

- State fund as controlling shareholder and corporate governance concerns; Kazakhstan sovereign and political risks;

- KAP currently does not report IFRS financials for all assets.

I or my affiliates may hold positions or other interests in securities mentioned in the Blog. Please see Disclaimer.

If you love the articles I write, follow my blog and never miss another investment opportunity!

1 thought on “„Atomic” Company NAC Kazatom – Feb. 2020 Update”