Large consumer opportunity. Neuromodulators (i.e. BOTOX®) are the most-performed minimally invasive cosmetic procedure in US with an estimated CAGR (2019-2025) of 9%. Daxi (see details below) is uniquely suited to expand the market. Daxi and BOTOX have nearly identical amounts of core active ingredient, botulinum toxin type A, in respective glabellar line dosage, with Daxi demonstrating 30% longer duration of effect ($2bn market opportunity);

Large therapeutics market opportunity with 11 approved therapeutic indications in neuromodulator category including cervical dystonia, plantar fasciitis and upper limb spasticity and other 700 potential indications ($2.5bn market opportunity).

Profile

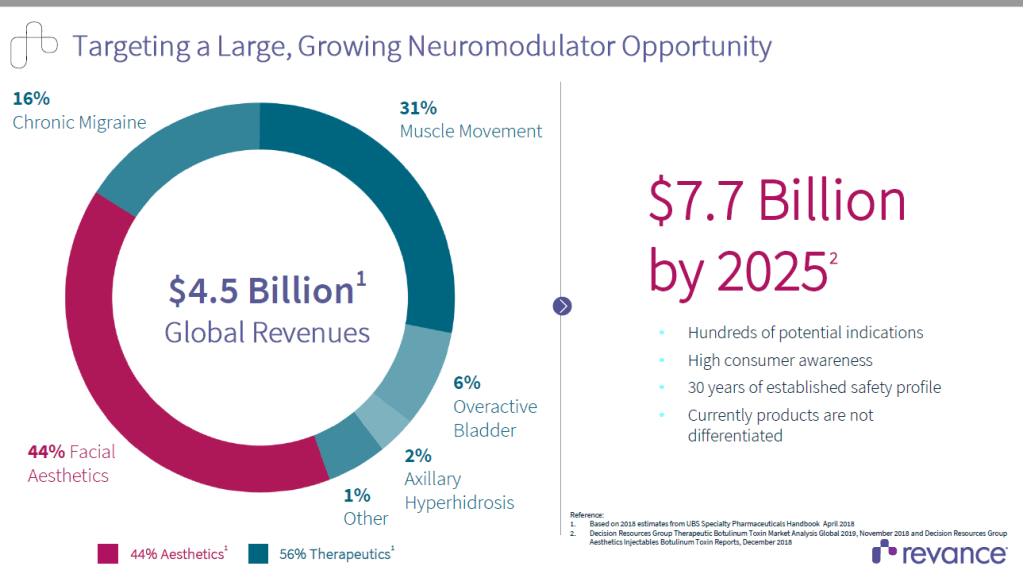

Revance Therapeutics (RVNC) is a Silicon Valley-based biotechnology company, pioneering new innovations in neuromodulators for aesthetic and therapeutic indications. RVNC is developing DaxibotulinumtoxinA (Daxi), a next-generation injectable botulinum toxin that would compete with Botox, Dysport and other smaller players in the $4.5bn global neuromodulator market.

RVNC filed for FDA approval of Daxi in November 2019 and is initially pursuing a label for glabellar (frown) lines with approval expected in 2020. According to preliminary studies Daxi duration of effect should be 6 months versus 3-4 month for BOTOX®, Dysport and similar.

DAXI is an investigational product. It is currently undergoing clinical studies for both therapeutic and aesthetic indications Revance is also evaluating Daxi in forehead lines and lateral canthal lines (crow’s feet), as well as in three therapeutic indications – cervical dystonia, adult upper limb spasticity and plantar fasciitis, with plans to study migraine.

Beyond DAXI, Revance has begun development of a biosimilar to BOTOX®, which would compete in the existing short-acting neuromodulator marketplace.

Please see below the 3 pillars of value creation and status of the product lines:

Source: Revance IR Presentation, Dec. 2019

Botulinum Toxin Market

Botulinum toxin is widely used in the treatment of various aging signs such as frown lines, forehead lines, square jaws, crow’s feet and others. Moreover, rising number of manufacturers in various economies will further augment market growth. Hence, growing influence of aesthetics among the population coupled with increasing number of manufacturers of various developed and developing countries will further propel market growth.

Increase in the prevalence of cervical dystonia and spasticity as well as number of cases of chronic migraine is expected to boost botulinum toxin market during the forecast period. As per the National Institutes of Health (NIH), in the U.S, more than 36 million adults are affected by migraine and it may lead to functional disability of health over time. Moreover, surge in adoption rate of non-surgical botulinum toxin procedures, due to their minimally invasive or non-invasive nature, is augmenting market growth over the forecast timeframe.

There are more than 7 million neuromodulator procedures per year and Botox enjoys a 76% market share in US with second player (Dysport) having a 15% market share.

Source: Revance IR Presentation, Dec. 2019

Valuation

There is a challenge to value a biotechnology company with no sales expected in the next 2 years for obvious reasons. My 12-month price target of $23 is based on a 4.5x EV/sales multiple applied to 2025 revenues and then discounted back at a 12% annual discount rate. According to some research, EV/Sales multiples in biotechnology sector are at (4.5x) and in aesthetics at (5.0x). I estimate the company will raise $120m in equity every year over next 3 years to fund product development and turn to profit starting year 2023. I see also a high probability that the company will be acquired in the 2-3 years at a premium. I assume approval of Daxi in 4Q 2020 and I project the product will capture 15% market share of cosmetic market and 5% of therapeutics market at peak in 2025. This should drive the company to reaching sales of $0.65bn by 2025. This would mean a target price of $29. I assume an 80% average probability of success of my above scenario hence I further applied a 20% discount to the target price arriving at US$23/share.

Investment Risks

Failure to receive FDA approval of Daxi, or FDA approval of Daxi but with an undifferentiated label (without longer duration of effect) vs. Botox;

Delays in product development and/or clinical trial failures that push back filing/approval timelines;

RVNC should be profitable following the approval and launch of Daxi, but until then the company will be dependent on the capital markets for financing.

I or my affiliates may hold positions or other interests in securities mentioned in the Blog. Please see Disclaimer.

If you love the articles I write, follow my blog and never miss another investment opportunity !

3 thoughts on “Botox Reloaded (Revance Therapeutics), Jan. 2020”